Unlock the Future of

DailyGameMoments leverages cutting-edge AI and quantitative strategies to maximize your crypto trading profits securely and efficiently.

Start Earning Now

Core Features

Based on Non-Price Factors

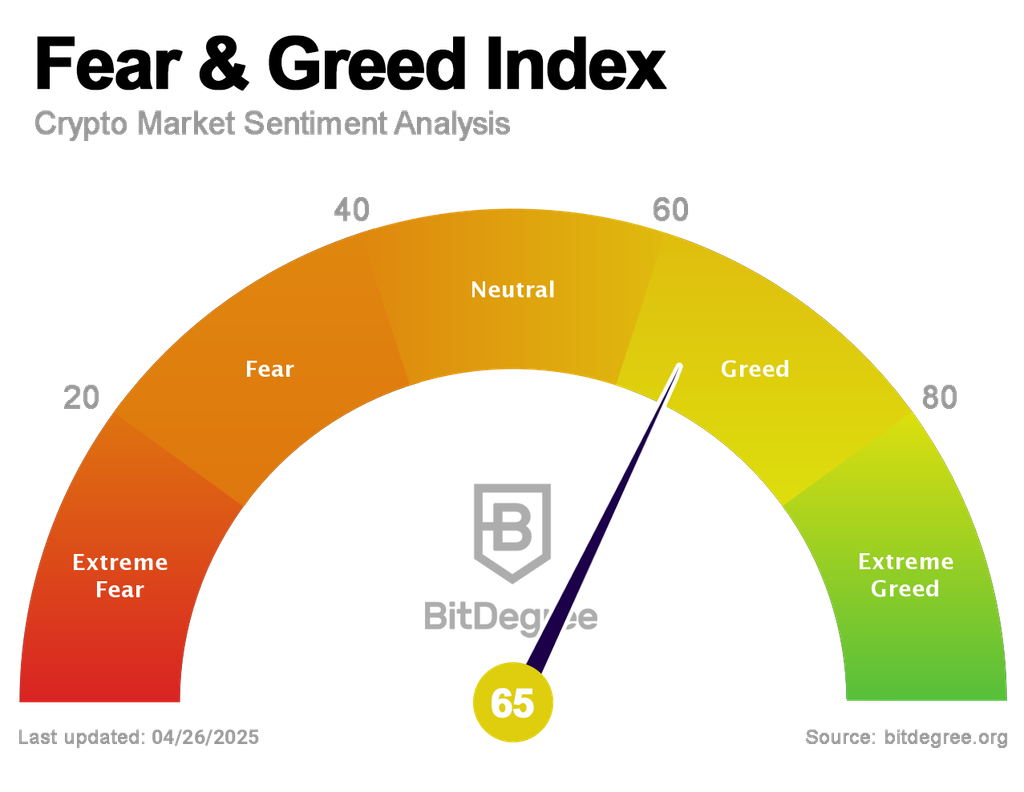

CoinGlass Insights

Track market sentiment with open interest, liquidation data, and funding rates. CoinGlass reveals what traders are really thinking behind the charts.

CryptoQuant Metrics

Explore exchange inflows, miner behavior, and whale movements. CryptoQuant delivers deep-chain analytics for early trend detection and smarter strategy timing.

Glassnode Signals

Leverage powerful on-chain indicators like NUPL, SOPR, and wallet activity. Glassnode transforms blockchain noise into clear investor signals.

Simple Steps to Success

Why Choose DailyGameMoments?

Cutting-Edge Technology

We employ the latest advancements in AI, machine learning, and quantitative analysis for superior trading performance.

Robust Risk Management

Sophisticated risk mitigation strategies are built into our algorithms to protect your capital in volatile markets.

Transparent Reporting

Track your performance with detailed, real-time reports and analytics directly on your dashboard.

Ready to Revolutionize Your Crypto Trading?

Join successful traders using DailyGameMoments to maximize your crypto profits.

Unlock Exclusive Access🔍 Find The Perfect AI Agent For Your Business

Our AI agents are designed to grow with your business ambitions. Whether you're just starting out or managing complex portfolios, we'll help you select the ideal solution.

Basic

- Autonomous task-handling

- Built-in tool access (web search, databases)

- Starter memory and logic flows

- Single-step or basic chained processes

- Easy upgrade path

Standard

- Custom deployment to your workflows

- Multi-step pipelines & orchestration

- Advanced memory & retrieval systems

- Monitoring, logging & optimization

- Production-level stability

- Recurring automations across departments

Enterprise

- Fully customized architecture

- Multi-agent frameworks

- Enterprise systems integration

- Robust governance & security protocols

- Scalable, real-time orchestration

- Digital transformation solutions

- End-to-end automation

All plans come with 24/7 support and regular updates

If you want to see a demo, click on the chat icon on the right-bottom corner of the screen. We support any languages.

For example, you can ask the agent for 🎯 products and 🤝 services available.