Congratulations to Zhujian Planning Media (Jilin) Co., Ltd. for breaking the record for the largest image formed by multirotor/drones. Can you guess how many drones were used? At Guinness World Records we want to show that everyone in the world is the best at something, and we’re here to measure it! Whether you’ve got the stretchiest skin, know the world’s smallest dog or want to create the largest human dominoes chain we want to hear about it. Here on the Guinness World Records YouTube channel we want to showcase incredible talent. If you’re looking for videos featuring the world’s tallest, shortest, fastest, longest, oldest and most incredible things on the planet, you’re in the right place.

The latest trading approaches for Solana (SOL) in October 2024 highlight its strong price momentum and positive outlook, driven by technical and fundamental factors.

Price Momentum: Solana is currently trading around $144, maintaining a solid upward trajectory with strong support levels at $140. The 50-day EMA is at $144.48, suggesting that a breakout above this level could lead to further bullish movement towards $160 and potentially $200 by the end of October. The Relative Strength Index (RSI) indicates neutral momentum, providing room for growth if buyer interest increases.

Technical Patterns: A symmetrical triangle formation on both daily and weekly charts suggests a potential breakout. If Solana can surpass the $155 resistance level, it is likely to target $180 and possibly $200, making this a critical price zone to watch. Conversely, failure to break above this could lead to a retracement toward $120.

Long-Term Outlook: Analysts are optimistic about Solana’s continued upward trend, supported by its strong technical foundations. Extended Fibonacci retracement levels show key price targets, with the possibility of reaching aspirational levels like $213 or even higher, depending on market conditions.

For traders, monitoring the breakout points and volume surges could provide good entry points for both short-term and long-term strategies. Keep an eye on resistance levels and support from indicators like EMAs and RSI for confirmation of the next significant move.

I Decoded The Liquidity & Manipulation Algorithm In Day Trading

Liquidation data can be highly informative when combined with metrics like volume, open interest, or funding rate. These three indicators help provide a clearer picture of market behavior and trader sentiment. Here’s how each works with liquidation data:

1. Volume and Liquidation:

Volume represents the total number of contracts or shares traded during a specific period.

Liquidations combined with high volume can signal a significant market move, as many traders are being forced out of their positions. For example, a spike in long liquidations combined with high selling volume often indicates a strong downward price movement, and vice versa for short liquidations.

Key Insight: When liquidations happen in high-volume conditions, it suggests strong conviction in the direction of the move.

2. Open Interest and Liquidation:

Open Interest (OI) represents the total number of outstanding contracts (positions) in a market.

Decreases in OI after large liquidations suggest positions are being closed, potentially marking the end of a strong move (e.g., a final shakeout).

Increases in OI with liquidations may indicate that new positions are being opened, often by more aggressive participants looking to capitalize on the forced liquidations of others.

Key Insight: A combination of high liquidations and falling OI could signal the exhaustion of a trend.

3. Funding Rate and Liquidation:

Funding Rate incentivizes traders to take long or short positions based on market imbalance.

Liquidations in the context of extreme funding rates are often a precursor to reversals. For example, if funding rates are extremely positive (indicating longs are paying shorts), and then a large number of long liquidations occur, it might signal that overly leveraged longs are being forced to exit, potentially triggering a downward move.

Key Insight: Funding rates help identify the positioning of the majority of traders. If liquidations occur with extremely skewed funding rates, it often means the market was over-leveraged in one direction, which could result in a price correction.

Summary of How They Work Together:

Volume + Liquidations: High liquidations with high volume = strong price moves with conviction.

Open Interest + Liquidations: High liquidations with falling OI = potential trend exhaustion; with rising OI = fresh participants entering.

Funding Rate + Liquidations: High liquidations with extreme funding rates = potential market reversal due to overly leveraged positions being wiped out.

Each of these indicators adds valuable context to liquidation data, and using them together can help you make more informed trading decisions.

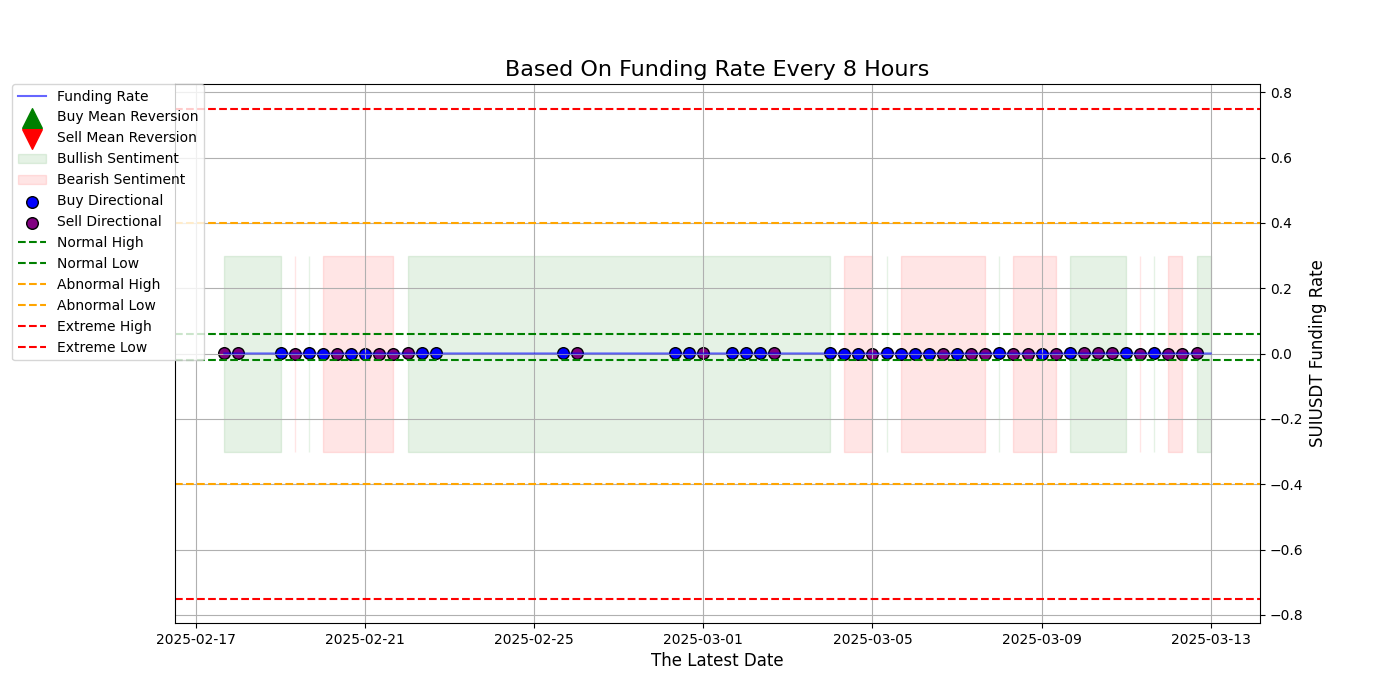

How it works: The funding rate can indicate market sentiment and extreme positions. If funding rates are very high or low, it suggests that one side of the market (long or short) is overleveraged. A mean reversion strategy involves entering positions expecting the funding rate to revert to more normal levels.

Goal: Bet against extreme funding rates, profiting from their eventual reversion as market sentiment stabilizes.

2. Market Sentiment Analysis

How it works: Funding rates can be used as a proxy for sentiment. High positive funding rates indicate bullish sentiment, while negative rates indicate bearish sentiment. Algorithms can use this information to adjust their trading strategies in line with prevailing market trends or take contrarian positions.

Goal: Capitalize on market momentum or sentiment shifts based on funding rate extremes.

3. Directional Trading Strategy

Goal: Align trades with the prevailing market direction as indicated by the funding rate or use it to enter contrarian positions when rates are extreme.

How it works: If the funding rate is positive and increasing, it suggests that long positions are dominating the market, while a negative and decreasing rate suggests shorts are prevailing. This information can be used in trend-following strategies.

import pandas as pd import numpy as np import random

Simulate funding rate data (Replace this with actual API data)

def simulate_funding_rate_data(n=100): dates = pd.date_range(end=pd.Timestamp.now(), periods=n, freq=’H’) funding_rates = np.random.normal(0, 0.01, n) # Random funding rates between -1% to +1% return pd.DataFrame({‘date’: dates, ‘funding_rate’: funding_rates})

Generate funding rate data

df = simulate_funding_rate_data()

Define trading strategies

class FundingRateStrategy:

def __init__(self, funding_rate_data, upper_threshold=0.005, lower_threshold=-0.005):

self.funding_rate_data = funding_rate_data

self.upper_threshold = upper_threshold

self.lower_threshold = lower_threshold

# 1. Mean Reversion Strategy

def mean_reversion_strategy(self):

"""

Mean reversion based on extreme funding rates. Enter contrarian positions when funding rates

are too high (short) or too low (long).

"""

signals = []

for index, row in self.funding_rate_data.iterrows():

if row['funding_rate'] > self.upper_threshold:

signals.append('Sell') # High funding rate -> Overleveraged long positions -> Short

elif row['funding_rate'] < self.lower_threshold:

signals.append('Buy') # Low funding rate -> Overleveraged short positions -> Long

else:

signals.append('Hold') # No trade signal

self.funding_rate_data['mean_reversion_signal'] = signals

# 2. Market Sentiment Analysis

def market_sentiment_analysis(self):

"""

Market sentiment analysis based on funding rate. Positive funding rates indicate bullish sentiment,

negative funding rates indicate bearish sentiment.

"""

sentiment = []

for index, row in self.funding_rate_data.iterrows():

if row['funding_rate'] > 0:

sentiment.append('Bullish')

else:

sentiment.append('Bearish')

self.funding_rate_data['market_sentiment'] = sentiment

# 3. Directional Trading Strategy

def directional_trading_strategy(self):

"""

Trade based on the direction of the funding rate. If the funding rate is increasing, it indicates a

bullish trend, otherwise, a bearish trend.

"""

signals = []

previous_rate = None

for index, row in self.funding_rate_data.iterrows():

if previous_rate is None:

signals.append('Hold')

elif row['funding_rate'] > previous_rate:

signals.append('Buy') # Funding rate is increasing, suggesting bullish trend

elif row['funding_rate'] < previous_rate:

signals.append('Sell') # Funding rate is decreasing, suggesting bearish trend

else:

signals.append('Hold')

previous_rate = row['funding_rate']

self.funding_rate_data['directional_signal'] = signals

def run_strategies(self):

"""

Run all strategies and generate trade signals.

"""

self.mean_reversion_strategy()

self.market_sentiment_analysis()

self.directional_trading_strategy()

return self.funding_rate_data

Instantiate the strategy class and run the strategies

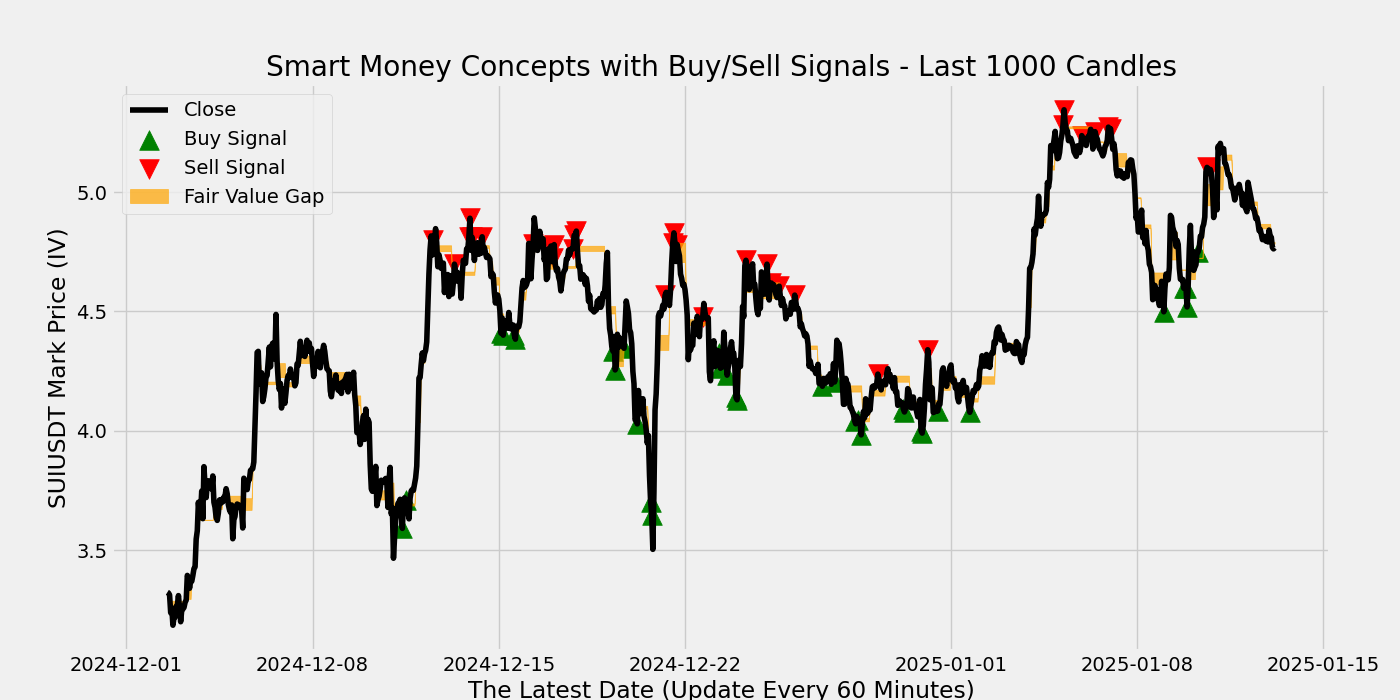

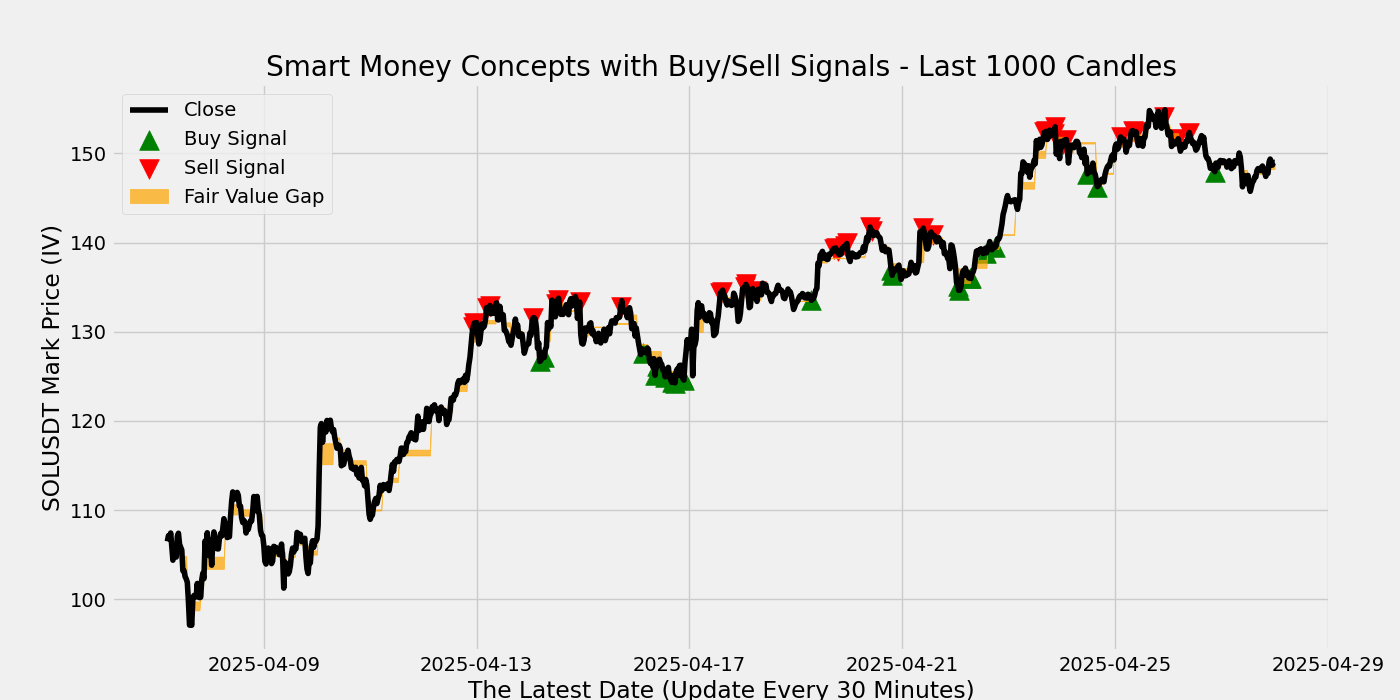

Smart Money Concepts (SMC) is a trading strategy that focuses on analyzing the behavior of institutional investors, such as banks and hedge funds, to gain insights into price movements in the financial markets. These institutional players, often referred to as “smart money,” have significant capital and the ability to influence price action. SMC aims to help retail traders understand how these large players operate, with the goal of following their moves to improve trading success.

SMC uses specific market structure principles to identify potential entry and exit points, such as:

Market Structure: Understanding trends, swing highs, and swing lows to determine market direction.

Liquidity: Institutions often target liquidity zones, such as stop-loss clusters, to execute large orders.

Order Blocks: These are price ranges where institutions accumulate positions before causing a significant price move. They can act as support or resistance zones.

Fair Value Gaps: Gaps left in price when the market moves quickly in one direction. These gaps often get “filled” as the price returns to those levels.

Equal Highs/Equal Lows: Institutional traders target these levels to trap retail traders and induce liquidity hunts.

SMC is commonly combined with other technical indicators or confluences, like the Relative Strength Index (RSI), moving averages, or supply and demand zones, to fine-tune entries and exits. Do you plan to implement this strategy in your trading system?

That’s great! Implementing Smart Money Concepts (SMC) can enhance your trading by focusing on institutional moves and key market structure points.

To integrate SMC into your system, you may want to define key concepts such as:

Swing Highs/Lows: For identifying market structure.

Order Blocks: Zones of accumulation and distribution.

Liquidity Zones: Areas where retail traders set stop-losses, often targeted by smart money.

Fair Value Gaps: Price imbalances that often get revisited.

Given your existing system that detects buy and sell signals based on specific confluences (e.g., Swing Lows, Bearish OB, and Equal Lows for buys), you could enhance it by:

Adding liquidity zones: Detecting where large liquidity might be resting (e.g., around equal highs/lows).

Identifying order blocks: Marking areas of consolidation or sharp movement that could indicate institutional buying or selling.

Tracking fair value gaps: Implementing logic to identify price gaps and potential retracement areas.

How would you like to approach the coding or strategy adaptation? Would you like suggestions for integrating any specific SMC principles with your current setup?

To integrate SMC principles with your existing setup, here’s how you can incorporate key concepts like liquidity zones, order blocks, and fair value gaps into your current detect_buy_sell_signals method. I’ll provide some pseudocode and ideas for how to adapt your strategy:

1. Swing Highs and Lows (Market Structure)

Since you are already using Swing Highs and Lows, you can improve their detection to mark trend reversals. For example:

pythonCopy codedef detect_swing_high_low(prices):

# Assuming prices is a list of price points

swing_highs = []

swing_lows = []

for i in range(1, len(prices) - 1):

if prices[i] > prices[i-1] and prices[i] > prices[i+1]:

swing_highs.append((i, prices[i])) # Swing High

elif prices[i] < prices[i-1] and prices[i] < prices[i+1]:

swing_lows.append((i, prices[i])) # Swing Low

return swing_highs, swing_lows

2. Order Blocks (OB)

Order Blocks are areas of consolidation before a price movement. You can detect them by identifying periods of small price range followed by large moves:

pythonCopy codedef detect_order_blocks(prices, threshold=0.01):

order_blocks = []

for i in range(3, len(prices)):

# Check for a small consolidation area (low volatility)

if max(prices[i-3:i+1]) - min(prices[i-3:i+1]) < threshold:

order_blocks.append((i, prices[i])) # Mark this as an order block

return order_blocks

3. Liquidity Zones

Liquidity zones are where stop-loss clusters are placed, often around equal highs/lows. Here’s a way to detect potential liquidity pools:

pythonCopy codedef detect_liquidity_zones(swing_highs, swing_lows, price_buffer=0.001):

liquidity_zones = []

# Liquidity zones around equal highs/lows

for i in range(1, len(swing_highs)):

if abs(swing_highs[i][1] - swing_highs[i-1][1]) < price_buffer:

liquidity_zones.append(('high', swing_highs[i][1])) # Equal highs

for i in range(1, len(swing_lows)):

if abs(swing_lows[i][1] - swing_lows[i-1][1]) < price_buffer:

liquidity_zones.append(('low', swing_lows[i][1])) # Equal lows

return liquidity_zones

4. Fair Value Gaps (FVG)

Fair Value Gaps occur when there’s an imbalance in price action. You can detect these gaps when there’s a large difference between candles:

pythonCopy codedef detect_fair_value_gaps(klines, gap_threshold=0.01):

fair_value_gaps = []

for i in range(2, len(klines)):

# Compare previous candle's close and current candle's open for gap detection

previous_close = klines[i-1]['close']

current_open = klines[i]['open']

if abs(current_open - previous_close) > gap_threshold:

fair_value_gaps.append((i, klines[i]['open'], klines[i-1]['close']))

return fair_value_gaps

5. Combining SMC Elements in detect_buy_sell_signals

You can now enhance your existing detect_buy_sell_signals method to include these SMC features. For example:

pythonCopy codedef detect_buy_sell_signals(prices, klines):

swing_highs, swing_lows = detect_swing_high_low(prices)

order_blocks = detect_order_blocks(prices)

liquidity_zones = detect_liquidity_zones(swing_highs, swing_lows)

fair_value_gaps = detect_fair_value_gaps(klines)

buy_signals = []

sell_signals = []

# Example logic for buy signals

for low in swing_lows:

if low in liquidity_zones and any(ob[1] < prices[low[0]] for ob in order_blocks):

buy_signals.append(low) # Buy signal at liquidity + OB confluence

# Example logic for sell signals

for high in swing_highs:

if high in liquidity_zones and any(ob[1] > prices[high[0]] for ob in order_blocks):

sell_signals.append(high) # Sell signal at liquidity + OB confluence

return buy_signals, sell_signals

Next Steps

Backtesting: You should test these concepts with historical data to fine-tune thresholds like order block consolidation ranges, gap detection limits, and liquidity zone buffers.

Visualization: Plotting these levels (order blocks, liquidity zones, fair value gaps) on charts will help in seeing how they align with price movements.

Would you like to focus on one of these aspects in more detail or get help with integrating them into your existing system?

Asynchronous programming and synchronous execution differ in how they handle tasks, particularly tasks that involve waiting for external events (like API calls, I/O operations, or database queries). Here’s a breakdown of the benefits and use cases for both approaches:

1. Asynchronous Execution

How it works:

In asynchronous execution, tasks that involve waiting (e.g., network requests, file I/O) can be started and then paused while the system waits for their completion. During that wait time, the system can perform other tasks instead of being blocked.

Benefits:

Non-blocking: Async operations don’t block the rest of the program. The program can continue executing other tasks while waiting for the I/O-bound task (like fetching data from an API) to finish.

Concurrency: Multiple asynchronous operations can run concurrently, improving performance. For example, you could request data from multiple APIs in parallel, and as each response is received, it can be processed.

Efficiency: Useful when dealing with I/O-heavy tasks such as file operations, database queries, or API calls. While one operation waits for data, others can proceed.

Scalability: Async code scales well, especially when you need to handle many tasks (e.g., handling multiple simultaneous API requests) without locking up your system.

Example Use Cases:

Fetching data from multiple APIs at once.

Web servers handling multiple incoming client requests.

Downloading files or large amounts of data while continuing to perform other operations.

Drawbacks:

More complexity: Asynchronous programming often introduces more complexity because you need to think about when tasks start, pause, and resume.

Harder to debug: Async operations can be more difficult to trace when things go wrong, as tasks aren’t executed linearly.

2. Synchronous Execution

How it works:

In synchronous execution, tasks are performed one at a time, and each task must complete before the next one starts. If a task involves waiting (e.g., reading from a file or making an API call), the entire program stops and waits until the task is done.

Benefits:

Simplicity: Synchronous code is easier to write, read, and understand because tasks are performed in a straightforward, step-by-step manner.

Deterministic: Each task completes in the exact order it’s written, making debugging and predicting program flow easier.

Useful for CPU-bound tasks: When operations are CPU-heavy (e.g., number crunching, data processing), synchronous execution is often sufficient because you’re not waiting for external events.

Example Use Cases:

Performing a series of calculations that don’t rely on external inputs.

Small-scale scripts that fetch data from a single source.

Programs where execution order is critical and where there’s no advantage to performing multiple tasks concurrently.

Drawbacks:

Blocking: If a task involves waiting (e.g., fetching data from an API), the entire program will be blocked until that task finishes. This can make the program feel slow or unresponsive.

Less efficient for I/O-bound tasks: When your program needs to perform multiple I/O operations (e.g., making API calls, file reads/writes), synchronous execution can be slow because tasks are processed one by one.

When to Use Which Approach

Asynchronous: Best for tasks that involve waiting for external operations, like network requests or file access, where you want to keep doing other things while waiting. It’s ideal when you’re building scalable systems (like web servers) that handle many requests at once.

Synchronous: Best for tasks that don’t involve waiting or where simplicity is important. For example, small scripts or programs where execution flow is straightforward or where operations rely on each other in a sequential manner.

Summary Table:

Feature

Asynchronous

Synchronous

Blocking

Non-blocking, tasks run concurrently

Blocking, tasks run one after another

Efficiency

More efficient for I/O-bound tasks (e.g., API calls, file reads)

Better for CPU-bound tasks (e.g., calculations)

Scalability

Scales well with many concurrent tasks

Scales poorly with waiting tasks

Complexity

More complex, requires async patterns like await

Simpler, easier to implement and debug

Use Cases

Web servers, APIs, real-time apps

Scripts, small tools, sequential operations

If your application has a lot of external API calls or I/O operations, asynchronous programming can greatly improve efficiency. However, for simpler tasks or programs that don’t involve much waiting, synchronous execution is often sufficient and easier to manage.

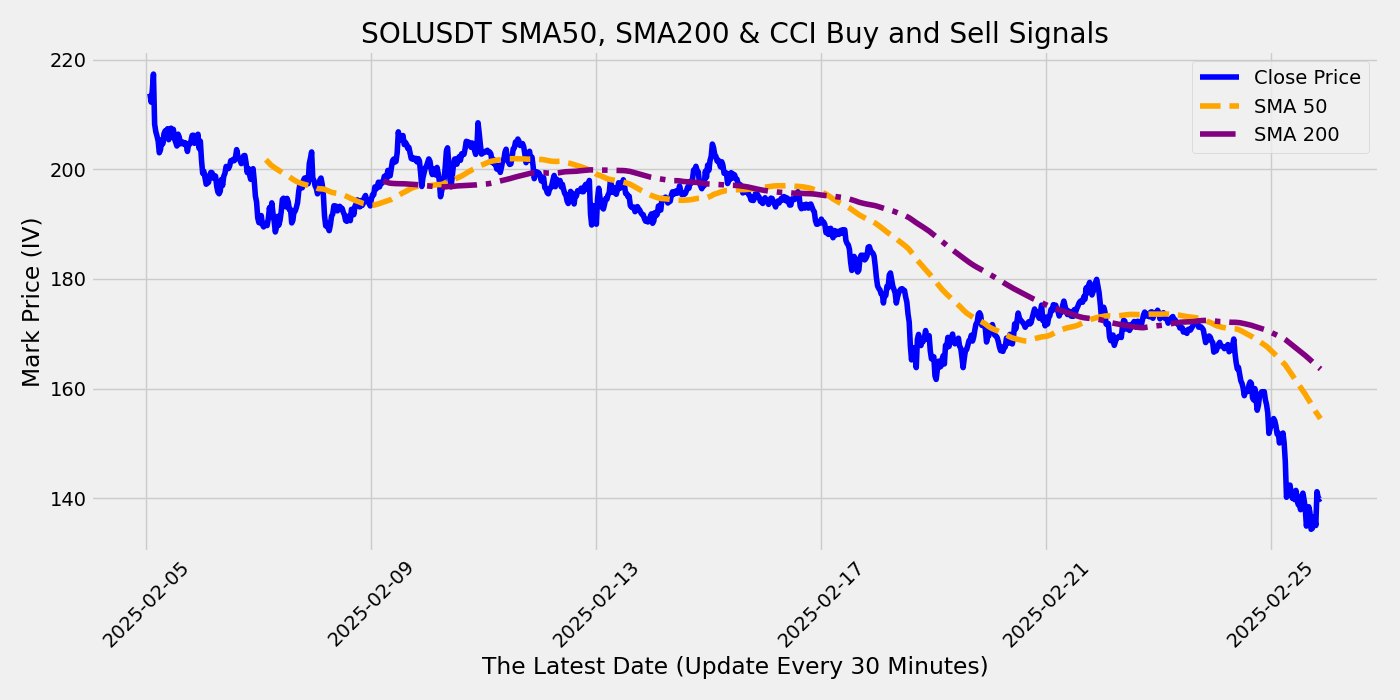

The CCI + EMA strategy combines two technical indicators: the Commodity Channel Index (CCI) and the Exponential Moving Average (EMA). This strategy uses these indicators to generate buy and sell signals based on the relationship between the price and the indicators, helping traders identify overbought/oversold conditions and potential trend reversals. Here’s a breakdown of how each component works and how they are used in this strategy:

1. Exponential Moving Average (EMA)

The EMA is a type of moving average that gives more weight to recent price data, making it more responsive to price changes compared to a simple moving average. The key role of the EMA in this strategy is to help identify the overall trend direction.

When the price is above the EMA, the market is considered to be in an uptrend.

When the price is below the EMA, the market is considered to be in a downtrend.

In this strategy, a 40-period EMA is typically used to smooth out the price data and help filter out short-term fluctuations.

2. Commodity Channel Index (CCI)

The CCI measures the difference between the current price and the historical average price over a specific period. It helps traders identify overbought or oversold conditions in the market. CCI values typically oscillate between +100 and -100, and signals are generated when the CCI moves above or below these levels.

A positive CCI value (above 0) indicates that the price is trading above its historical average, which may signal strength.

A negative CCI value (below 0) indicates that the price is trading below its historical average, which may signal weakness.

In this strategy, multiple CCIs (e.g., CCI 50, CCI 25, CCI 14) are used to capture different timeframes, providing a more comprehensive view of the market.

3. Buy and Sell Signal Logic

The strategy generates buy and sell signals based on the relationship between the price, the EMA, and the CCI values.

Buy Signal

A buy signal is triggered when:

The price is above the 40-period EMA, indicating an uptrend.

All CCIs (e.g., CCI 50, CCI 25, CCI 14) are positive (above 0), indicating that the market is in a strong bullish condition.

This combination suggests that the market is in an uptrend and experiencing strong buying pressure, making it a good time to enter a long position.

Sell Signal

A sell signal is triggered when:

The price is below the 40-period EMA, indicating a downtrend.

All CCIs (e.g., CCI 50, CCI 25, CCI 14) are negative (below 0), indicating that the market is in a strong bearish condition.

This combination suggests that the market is in a downtrend and experiencing strong selling pressure, making it a good time to enter a short position.

4. Adjusted Buy and Sell Signals

To reduce noise and false signals, the strategy can be refined by using “adjusted” buy and sell signals. This adjustment involves:

Confirming that the opposite signal has occurred multiple times before triggering a buy or sell signal. For example, a buy signal is only triggered after 3 consecutive sell signals, and vice versa.

This ensures that signals are only generated after a clear trend reversal is evident, improving the reliability of the signals.

Summary of the Strategy:

Buy signal: When the price is above the EMA and all CCI values are above 0, indicating a strong uptrend.

Sell signal: When the price is below the EMA and all CCI values are below 0, indicating a strong downtrend.

Adjusted signals: Buy and sell signals are refined by confirming that multiple opposite signals have occurred before triggering a new signal, reducing false signals.

This strategy helps traders enter trades when the market is trending strongly, while using the CCI to avoid entering trades during sideways or weak market conditions.

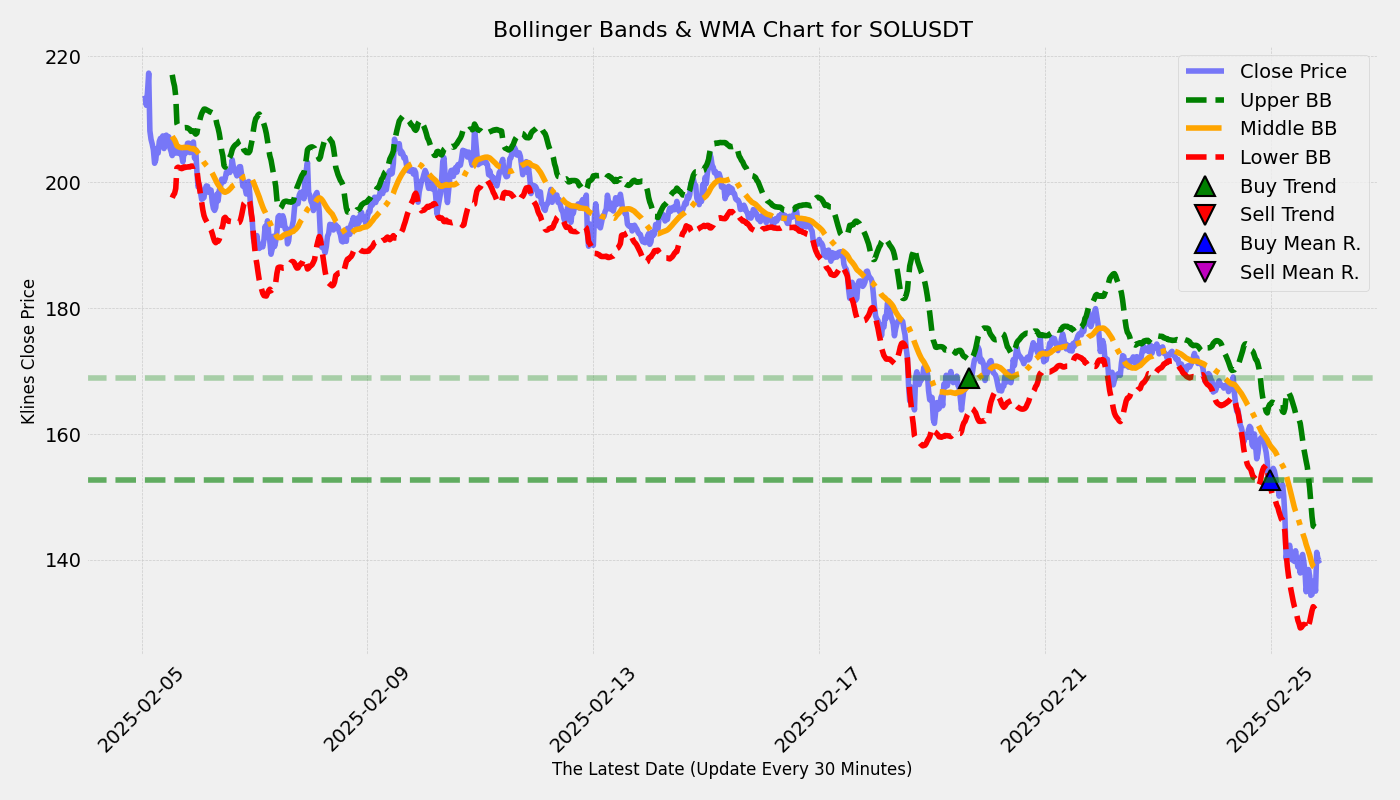

The Bollinger Bands indicator is a powerful tool used in both mean reversion and momentum trading strategies. By measuring the volatility of the market, it creates a band around a moving average that can indicate overbought or oversold conditions, as well as the strength of a trend.

1. Mean Reversion Strategy:

Idea: Prices that deviate far from the moving average (i.e., touch or breach the bands) will revert to the mean (the moving average).

Strategy: If the price touches or breaks below the lower Bollinger Band, it’s a potential buy signal (oversold); if it touches or breaks above the upper band, it’s a potential sell signal (overbought).

2. Momentum Strategy:

Idea: When prices break out of the Bollinger Bands, it may indicate a strong trend is developing.

Strategy: A breakout above the upper band indicates bullish momentum (buy signal), and a breakout below the lower band indicates bearish momentum (sell signal).

Python Implementation of Bollinger Bands for Both Strategies:

Here’s how you can calculate and use Bollinger Bands for both Mean Reversion and Momentum Trading strategies.

# Apply Mean Reversion Strategy

df = mean_reversion_strategy(df)

# Apply Momentum Trading Strategy

df = momentum_trading_strategy(df)

# Save to SQLite (if needed)

save_dataframe_to_sqlite(df)

return df

Fetch your data, then pass the data

Explanation:

Bollinger Bands: Calculated with a moving average and standard deviation over a defined period (usually 20 periods), with UpperBand and LowerBand representing volatility thresholds.

Mean Reversion Strategy: The logic identifies signals where the price touches or moves outside the lower band for a buy signal (indicating oversold conditions) and outside the upper band for a sell signal (indicating overbought conditions).

Momentum Strategy: The logic here captures when the price breaks out of the Bollinger Bands—above the upper band for a buy signal (indicating bullish momentum) and below the lower band for a sell signal (indicating bearish momentum).

Saving to SQLite: The resulting DataFrame is stored in an SQLite database.

Parameters You Can Adjust:

period=20: This is the number of periods over which the moving average and standard deviation are calculated. You can experiment with different values depending on your strategy.

std_dev=2: This is the number of standard deviations that defines the width of the Bollinger Bands. Standard practice uses 2 standard deviations, but you may adjust this to increase or decrease the sensitivity.

Integration:

You can further customize this strategy to incorporate it into your existing trading algorithms by integrating it with other signals (such as RSI or SuperTrend) to confirm trades.

Add filtering or more complex logic to refine your buy/sell conditions.

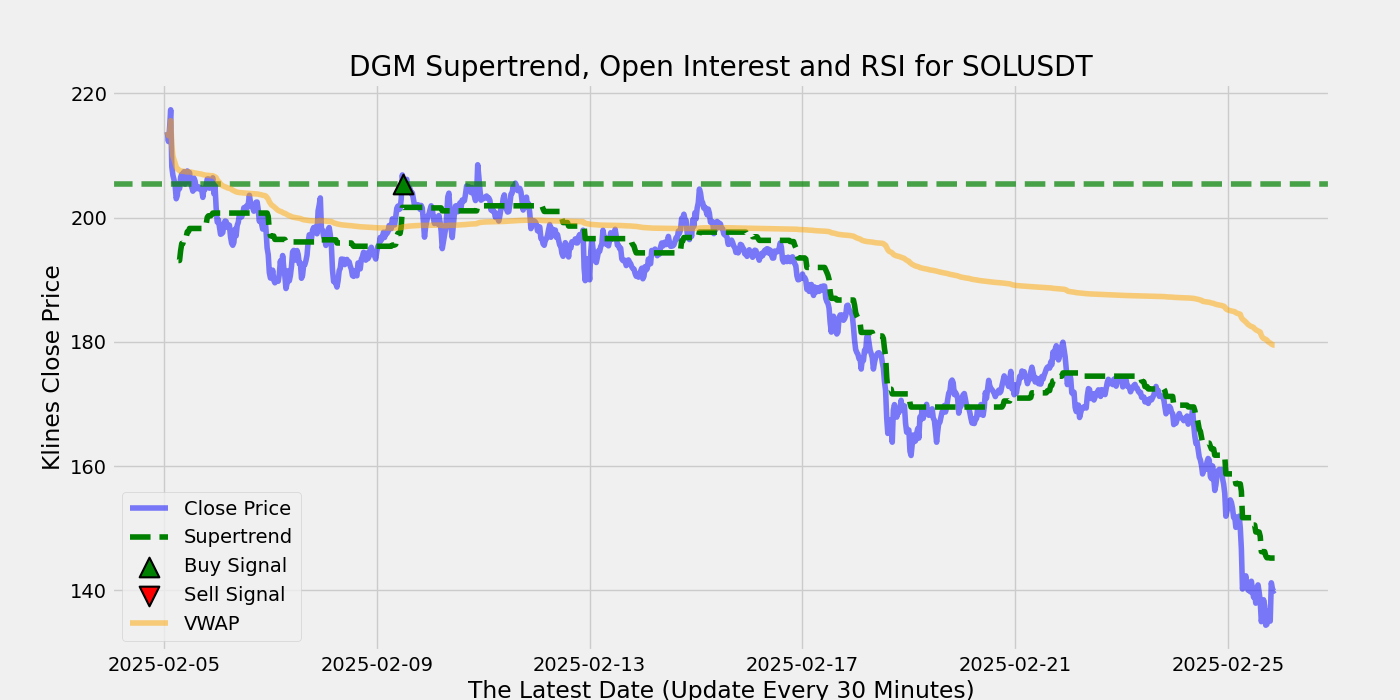

SuperTrend, Open Interest, and RSI. Each of these indicators can provide valuable insights when used in technical analysis for trading. Here’s a brief overview:

SuperTrend:

A trend-following indicator that can help identify the general market direction and potential buy or sell signals. It typically consists of a “trend line” overlaid on the price chart and changes direction when a certain threshold is reached.

Formula: SuperTrend is usually calculated based on the Average True Range (ATR). The basic idea is to compute a baseline and adjust it with a multiple of the ATR.

Refers to the total number of open contracts for a particular futures or options market. It can help traders understand the strength of a trend, as increasing open interest can indicate that new money is flowing into the market, while decreasing open interest may indicate profit-taking or trend reversal.

Relative Strength Index (RSI):

A momentum oscillator that measures the speed and change of price movements. The RSI oscillates between 0 and 100, typically using 14 periods. Readings above 70 are considered overbought, and readings below 30 are considered oversold.

Formula: RSI = 100 – [100 / (1 + RS)], where RS is the average gain of the up periods during the specified time frame divided by the average loss.

def calculate_rsi(df, period=14): delta = df[‘Close’].diff(1) gain = np.where(delta > 0, delta, 0) loss = np.where(delta < 0, -delta, 0)

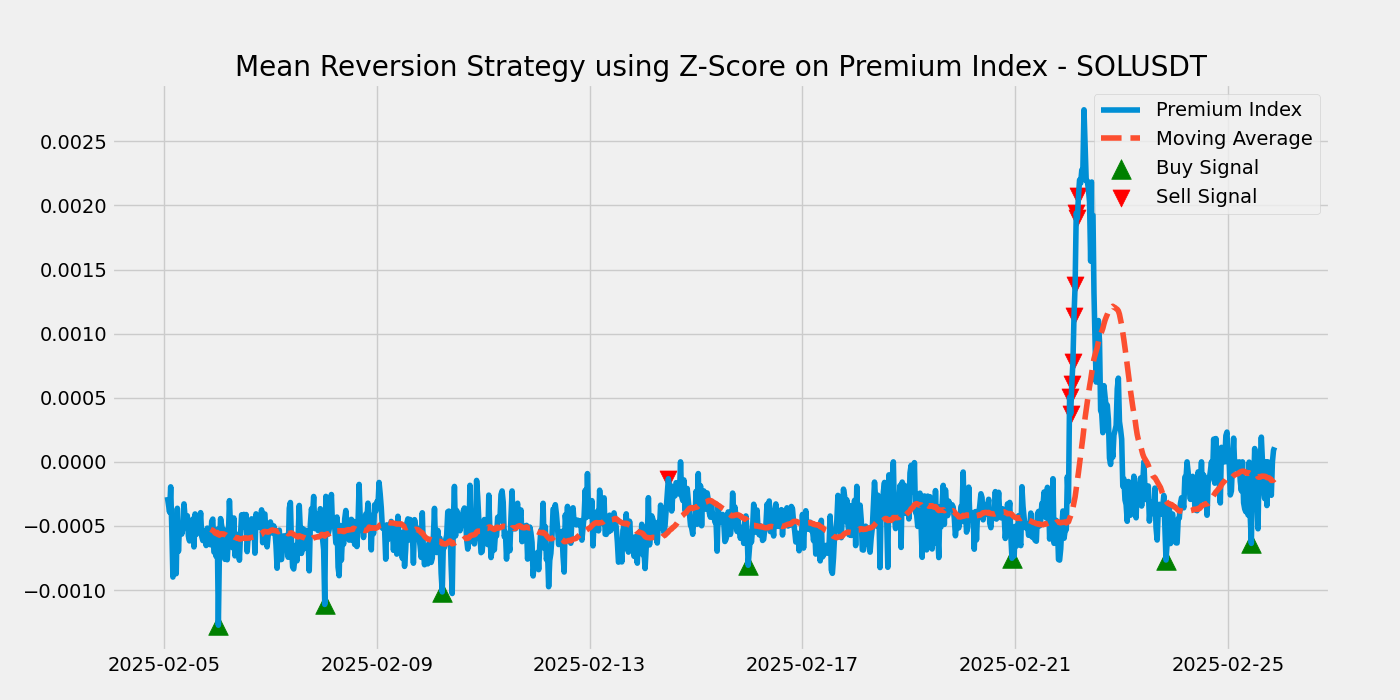

Mean Reversion strategies are based on the idea that prices and other financial metrics tend to revert to their historical mean or average level over time. Using the Z-Score in a mean reversion strategy helps identify when the premium index is significantly deviating from its historical mean, signaling potential trading opportunities.

Mean Reversion Strategy Using Z-Score on Premium Index

Here’s a step-by-step guide to implementing a mean reversion strategy using the Z-Score of the premium index:

1. Fetch and Prepare Historical Data:

Retrieve historical premium index data from your source (API, database, etc.).

2. Calculate Mean and Standard Deviation:

Compute the mean and standard deviation of the historical premium index values.

3. Calculate Z-Score:

Determine the Z-Score for the current premium index value using the historical mean and standard deviation.

4. Define Trading Signals:

Based on the Z-Score, create rules to generate buy or sell signals:

Buy Signal: When the Z-Score is below a certain threshold (e.g., -2), indicating the premium index is significantly below the mean and might revert upwards.

Sell Signal: When the Z-Score is above a certain threshold (e.g., 2), indicating the premium index is significantly above the mean and might revert downwards.